Money on the Left is proud to publish a remastered version of our third episode with Fadhel Kaboub, now with a new transcript and art. Kaboub is associate professor of economics at Denison and President of the Global Institute for Sustainable Prosperity. In our conversation, Kaboub outlines a new critical approach to postcolonial political economy, arguing that re-gaining fiscal agency is a crucial next step for postcolonial nations hoping to achieve social, economic, and environmental justice. We talk specifically and at length about the CFA franc currency union, a system with violent colonial roots that continues to constrain the economic and political agency of its member states in West and Central Africa.

Visit our Patreon page here: https://www.patreon.com/MoLsuperstructure

Music by Nahneen Kula: www.nahneenkula.com

Transcript

This transcript has been edited for readability.

Scott Ferguson

Fadhel Kaboub, welcome to Money on the Left.

Fadhel Kaboub

Thank you. Thanks for having me.

Scott Ferguson

So I was wondering if we could start by having you tell us about your personal background and also your intellectual training.

Fadhel Kaboub

For my personal background, I grew up in the Middle East, in Saudi Arabia, in Tunisia. I did most of my higher education in Tunisia, and moved to the US for grad school. I went to the University of Missouri in Kansas City, where I did my master’s and PhD. The timing is relevant here. I started in January 2000, which was about six months after the Center for Full Employment and Price Stability was inaugurated in Kansas City.

This was the research center that was directed by Matt Forstater with the research team, including Randi Ray, Stephanie Kelton, Povlina Chernova, and then later on, Fred Lee joined the economics department, and it was just becoming a hub of post Keynesian and institutional economics. It was just a wonderful place to be at in terms of grad school, summer programs and just intellectual development. After my PhD, I went into teaching. Even before finishing my dissertation, I was teaching a little bit in Kansas City, which was a great experience. But then eventually, started teaching full time tenure track at Drew University in New Jersey and then moved back here to Denison University in 2008 on a tenure track and have been here since then — almost ten years now.

About four years ago, Matt Forstater and myself had the opportunity to launch the Binzagr Institute for Sustainable Prosperity, which is a public policy think tank, an independent think tank based here in the US. From the beginning, we wanted to make sure that it’s an international organization in terms of our coverage. We wanted it to be “not your traditional academic think tank” that publishes papers primarily for academics.

We wanted this to be solutions oriented and accessible to the media, accessible to grassroots organizations, and accessible to policymakers. We still do publish academic papers, but we’re trying our best to move into policymaking and policy communication with the general public and with the media and with grassroots organizations. Also, from the beginning, we wanted this not to be purely an economic policy institute.

We wanted this to be an interdisciplinary organization, because we do recognize that the biggest problems that we face as a society are complex, multifaceted issues and require multi-pronged solutions and economics by itself just doesn’t have enough breadth and capacity to deal with these issues. For example, when you think about climate change, there’s obviously an economic dimension to it, there’s a political dimension, there’s an ethical dimension, there’s a scientific dimension to it. So you can’t just try to address it from an economic policy standpoint and expect good results. We wanted this to be an interdisciplinary institute, but also we wanted to have a solid foundation for what the focus of this institute would be.

Fadhel Kaboub

Because of our background in both Keynesian institutional economics and our interest in MMT, the job guarantee program was clearly going to be one of the central issues that we deal with because we do believe this is a policy framework that kind of challenges the mainstream of public policy, the mainstream of the profession, to rethink how we address social and economic problems.

We also wanted this to be an invitation to our friends in the environmental movements and social justice movements, who are progressive on every single aspect of their work except they fall in the trap of, “if we’re going to deal with climate change, how are we going to pay for it?” That’s where they fall into the traditional economic policy framework that says, “well, we need to tax the rich to do it, or tax pollution to do it, or the government is broken. We don’t have resources. So we can’t be as ambitious in our fight against climate change or fight against injustice or fight against whatever our social issue is.” In response, we wanted to connect with progressive lives and other disciplines and build bridges that allow other disciplines to be liberated and empowered by what MMT and the Job Guarantee framework has to offer.

That’s really the vision. During the last four years we’ve been building those bridges with people in the humanities, legal scholars, philosophers, political scientists and people from all kinds of different disciplines. It’s just the beginning. This is a long process, obviously, of undoing a lot of the damage that has been done in the economics discipline in academia in general, but especially in public policy.

Now, I get this question all the time, “like, are you really going to undo the neoliberal political economy with this institute?” The idea is, “yes,” but also it’s a recognition that we’re a few decades late and several hundred million dollars behind. We’re outnumbered and understaffed when it comes to this, but that’s what it takes.

It takes building a compelling narrative based on solid academic research and engaging with people at the public policy level, at the grassroots level. I truly believe that the way the neoliberal movement was able to dominate, starting in the 70s and 80s, is not because they won academic debates in journals or in conferences.

It’s because they were able to put together a political narrative that was compelling and hit a nerve when it came to the US public at the time in the 70s, especially in the US, and in the UK also. The Friedmans and Hayeks lost all the academic debates, but they won the political narrative. They had charismatic leaders who took it to the streets, so to speak. They had multi-million dollar-type of foundations behind them to push for the media and PR movement that shifted the culture. I believe that’s how we’re going to counter this. It’s not going to be just academics sending rejoinders to each other’s papers. We’ve done that. It’s just going to stay in those circles. I think this has to be taken to the public domain. If we’re going to build a movement, a social movement, it has to be accessible to the general public. It takes a lot of education, and it takes a lot of really engaged citizens who are looking for alternatives and willing to learn the alternative.

By “learning,” I don’t mean in the academic sense, I mean “learning” in the colloquial sense of the term that you are able to say what you believe in and articulate how it can work in nonacademic terms and get other people who are completely disconnected from the political sphere to be inspired and to believe in a different way of doing things and to vote accordingly and to act accordingly. That’s really that’s really the vision that that we have and we recognize it’s ambitious, but we’re really seeing bits and pieces of this happening. I’m optimistic.

Scott Ferguson

As a follow up question, which takes us back to the beginning, I’d like to hear, if you don’t mind, a little bit more about growing up in the Middle East and Tunisia and Saudi Arabia and what your own process of politicization has been, and maybe when and where, and what that might bring to the Modern Money Project that’s different than what we get from other perspectives within that project.

Fadhel Kaboub

Thank you for the question. I’ve been reflecting on this for a few years now in terms of how my own thinking has been influenced by my upbringing. So, as I said, I grew up in Saudi Arabia and Tunisia. My mother’s side of the family are from Saudi Arabia and my father’s side of the family is from North Africa, Tunisia, and to some extent, Algeria. Thinking back on that experience, I really didn’t grow up with the very powerful, overwhelming sense of national identity. I knew it was there because I can see it in my cousins on both sides of the family: the flag and the national anthem and the love for the football team and all that.

I mean, I love the football teams. I like both, and I like Brazil and Argentina and other things. But there’s this thing that I noticed from the beginning that, “my goodness, people are crazy about the flag.” I never understood what it was, I just thought, “well, this is their team and they like it.” Growing up later, you realize that this was designed when you think about all the post-colonial states in Africa and the Middle East and other places, governments didn’t really have much of a legitimacy. It had to be earned.

It had to be created. In the case of Tunisia, for example, there was a national leader. The independence leader was a very charismatic person, but there were no precolonial national borders that were well defined to go back to. The border had to be created and confirmed and protected. Then the national identity in terms of language and religion and culture, because a lot of these places were pretty ethnically diverse. National identity was, in most post-colonial countries, created and enforced through music, through culture, through sports, and with the idea of what you would call here in the US, patriotism, or in other countries called nationalism.

There’s that negative connotation about nationalism, but to me it’s the same thing. I grew up not feeling sucked into that understanding of national identity. For me, it was, “this is a country, this is another country.” I never grew up with the sense that I will die for my country, because which country will you die for? Plus, I come from a family that’s also very international. It wasn’t like everybody on one side of the family was Saudi, and everybody on the other side of the family was Tunisian. We had, through intermarriage, people from Egypt and Palestine and Algeria and Morocco and Lebanon. It wasn’t like we had only 1 or 2 national identities that the family had to pledge allegiance to. It’s an unusual family to begin with. To me, that sort of came back to me later in my career, reflecting on and starting to really think about what national identity means and how powerful it can be in war and peace conflict in terms of dividing nations.

I take comfort in knowing that I experienced that at an early age and sort of began to reflect on it throughout my life and now I understand how powerful those ideas can be. I can understand when I hear or see people who feel very strongly about a flag or their military or the nation because I know it’s nothing personal. It’s just, you’re born into it and you’re brainwashed into it, and to some extent, there is nothing wrong with that. The only part that is is when it comes to “it’s us against them,” and it begins to divide people because of the difference of their religion or their color and things like that. A healthy dose of patriotism is reasonable. I’m not against that. Loving a football team is great and loving the national anthem is great, but when it turns you against other people, it becomes problematic.

Maxximilian Seijo

It’s really interesting, when you talk about your experience of growing up in post-colonial Tunisia and Saudi Arabia and experiencing nationalism. What it makes me think of is the way that post-colonial theorists tend to begin from the presumption that you’ve already alluded to, that even though relations of explicit political colonization seem to end during the 19th and 20th centuries, there are unjust processes of economic, social, cultural or colonization that remain strong. They sort of frame this and focus on history in the politics of money and foreign denominated debt. I was wondering if we can circle that experience back to MMT. If you could help elucidate how MMT can imagine reframing this critical project in terms of political economy and then perhaps even a socio-cultural critique that you already started to tease out.

Fadhel Kaboub

Let me take this back to my undergraduate studies in Tunisia, where I studied economics. It’s a French, post-colonial education system. It’s not liberal arts. There is no general education. It’s four years of economics and nothing but economics, and a little bit of accounting and business and lots of math.

There isn’t really anything “political economy” per se. The closest we got to political economy was the History of Economic Thought class, which was the best thing I remember taking. It was a breath of fresh air in those four years. To link it back to your question, the reason why I wanted to go back to this is because during those four years of economics that I studied in Tunisia, we didn’t learn anything about the Tunisian economy.

This is not because it was neoclassical economics and neoclassical economics didn’t teach you anything about the real world. No, it wasn’t the case, actually. We had great teachers who are sort of post Keynesian-ish, institutionalist, kind of French influence, which was great, but this was strictly political. I learned so much about the Japanese economy, so much about the American economy, so much about the French economy. We even went to a couple of the professors after a class, “can we just have one lecture about the Tunisian economy or economic history?” We did take an economic history class, but it was about the Great Depression in the US and Japan and everything else. The professor said, “Leave me alone. What do you guys want? Go away.” It’s because they didn’t want to get into anything that will cross into politics. There were undercover police officers in the classrooms and on campus listening in because the history of protests in Tunisia was either the labor movement or the student movement or both converging together.

When you were going to police the population, you police the universities first. The campus where I studied was not like American campuses. This was a gated campus and guarded by the riot police. Actually, the riot police had one of their headquarters on campus, full gear. Those were the visible guys. The invisible ones were in the classroom. That’s why the professors didn’t even dare to talk about anything that has anything to do with the Tunisian economy. What I ended up learning about the Tunisian economy, I learned in Kansas City after I left. What I knew about the Tunisian economy was just observing and living in it and just trying to piece things together on your own or with a few friends, people you trusted to talk about political economy at the time.

What I ended up learning academically, intellectually was just after I moved to the US. I just started diving into books and archives and whatever I can find through interlibrary loans to read everything that there was to read about Tusinian economy. I ended up doing my dissertation on Tunisia. There’s an important link to your question here about the post-colonial thing. There’s been an intellectual movement in the last few years, both in Tunisia and other parts of Africa in particular, trying to essentially decolonize the curriculum, because the curriculum itself, in any discipline, was a Eurocentric curriculum. This is true in the US too, but especially in the Middle East because when you think of the history of any intellectual discipline, economics, for example, you read Schumpeter’s History of Economic Analysis, he talks about the great gap because first there was the Greeks and then the Romans, and there was nothing for 500 years. Then all of a sudden, the enlightenment happens. You read the history of science books, same thing.

There were the Greeks and the Romans, and then there was nothing and then all of a sudden science emerged in Europe. That’s taught in every single textbook, including in the Middle East and Latin America, India, and Africa. That’s how the Eurocentric narrative dominates and ends up colonizing the curriculum of supposed post-colonial, independent nations. You’re already put into an intellectual position of inferiority and economic position inferiority and a political position of inferiority and subordination, but you have your own flag and you have your own national anthem and you have your football team to celebrate. You see what I mean? That happens to serve the interest of the political leadership, because in most post-colonial nations, that political leadership didn’t really democratize the nation. They took over the exact same top down bureaucratic hierarchy, which was a dictatorial hierarchy created by the colonizers. It’s just now staffed by nationals who love the flag. You see what I mean? So, it was still a political and bureaucratic institutional structure of subordination, but now led by the charismatic independence movement leader, now turning into a dictator. I hope this answers your question in some sense, but that’s how I read it for several years now in terms of reflecting back, and talking to academics today and Tunisian former professors who understand that this is really part of the narrative. In addition to the fact that linguistic domination has been there from the beginning and constantly enforced by colonial interests.

Tunisia is an Arab country, but the main language of instruction academically is French. Over time, that came at the expense of losing the linguistic quality of the Arabic language in professional settings and in academic settings. When you lose a language, it’s really hard to undo that.

Maxximilian Seijo

I’d like to pick up on your point about the kind of organizational legacy of colonialism and subordination. In adopting the colonial governance scheme that was imposed on other nations in the global South, these countries, in large part to do with the intergovernmental organizations that made sure of this, kept to this idea that they still depended upon United States or France or countries across the globe from the global north for loans and debt so that they could finance their militaries and their often corrupt dictatorships. I was wondering if you could talk specifically about the way in which MMT reframes that discussion around foreign debt and monetary sovereignty.

Fadhel Kaboub

For the followers or the listeners of the podcast who are not very familiar with the MMT framework, I’ll just define the four basic bullet points that will be relevant to this conversation. From an MMT perspective, a country has full monetary sovereignty or full financial sovereignty. In a colloquial sense, full financial independence if the following four conditions apply. The first two conditions are pretty straightforward and easy for any country to do, the third and fourth are more problematic for post-colonial and developing countries in general.

The first condition is a country prints its own currency, or issues its own currency, and it’s the monopoly issuer of that currency. Most post-colonial governments, the first thing they do — not the first thing — but a couple of years after independence usually, is they start issuing a national currency and they start taxing the population in the national currency. That’s the first and second condition of monetary sovereignty and most countries can do that. The third condition is for a country to issue debt or issue bonds or treasuries that are only denominated in the national currency. That’s where a lot of developing countries start to lose their monetary sovereignty, because they start issuing both categories: bonds that are denominated in the national currency, but also bonds that are denominated in US dollars or Japanese yen or British pounds or any kind of foreign currency.

That part of their bond issuance becomes their external debt and it’s a real burden on those governments because it’s not something that they can finance internally. It means that you have to somehow generate export revenues in excess of what you would need to pay for your imports in order to be able to pay the debt, service the debt, and pay principal and interest.

That relates to the fourth condition, which is the fixed exchange rate policy that a lot of developing countries use. So, in order to have full monetary sovereignty, you want a flexible exchange rate. In other words, you don’t want to stand ready with excess reserves of dollars or euros or pounds to defend a particular exchange rate. That happens because the third condition is often violated. Meaning, if countries have a lot of external debt and have a lot of pressure on their exchange rate to devalue, that becomes a very politically and socially sensitive issue. If a small country faces a devaluation of their currency and they need to import food or fuel or energy or medicine or whatever necessities, it means with the devalued currency, all of those things now will cost more.

They’ll be importing inflation; food inflation, energy inflation and medical expenses inflation. That turns into social unrest in many cases. That’s why a lot of these developing countries end up borrowing even more every year in order to defend a fixed exchange rate level, which would prevent that inflationary pressure from actually turning into political and social unrest.

To me, that’s a very important starting point and that’s really the important lens that MMT has offered, to see with clarity why the issue of debt is problematic. Before the MMT lens, people knew that debt was an issue, but there was a confusion or conflation of the national debt as a domestic currency denominated debt versus external debt denominated in foreign currencies.

I think MMT tells us that the portion of the debt that’s done denominated in the national currency can always be managed, and there are ways of dealing with it. But the external portion is what really puts pressure on countries and that’s, personally, what led me into researching the root causes of the external debt and looking into potential solutions to address those root causes. Everything else we’ve seen in the last 30 or 40 years is really Band-Aid solutions, it’s really just rescheduling, stretching out the debt payments or getting more external debt and kind of feeding into the same problem that’s just been compounding over the years.

Scott Ferguson

So can you walk us through what it might look like for a country that is heavily indebted, has a weak productive infrastructure, is not, as you say, sovereign in food and or energy. What might be done in a situation as dire as that?

Fadhel Kaboub

First, I’ll tell you what is being done and how things got worse, starting with the post-colonial era and then we can talk about how to get out of it. Going back to the early post-colonial era, you have to recognize that the economic infrastructure of most of these countries was built up because colonialism lasted for decades, or over a couple of centuries in some cases. So, during that time, there was infrastructure built and there was a process of economic development and economic activity happening, which a lot of people confuse with economic development in the purest sense of the term. But, when you look carefully at what kind of infrastructure and what kind of economic development was done, you realize that it was very extractive.

Any kind of infrastructure that was built was purely for the purpose of extraction of wealth and extraction of resources. For example, Tunisia’s is a very interesting case, and you can look at the map of most African countries and post-colonial countries. Just look at the map of the railroads, the map of the roads, and then identify where the major mines are, where the major resources are and where the ports are built. It’s just direct straight lines from the mining town, straight through the rest of the country to the ports. The railroads are also built like that. The roads are built like that. So Tunisia, for example, you find a lot of east-west roads and east-west railroads, but nothing going north-south because there is no reason for people to go north-south. Once you’re independent as a country, you’re not going to sit down with the rest of the population and say, “okay, so this was a big mess, this colonialism. Let’s now start over again and let’s scrap all of the infrastructure and build it the way we really want it to be built.” It wasn’t like that.

Day one after independence, you continue doing the exact same thing you did before independence. You continue digging the same mines, loading on the same railroads to the same ports, and shipping them to the same customers in France or in Italy and other places. The post-colonial economic infrastructure continued to be built according to the colonial economic infrastructure.

It was a continuation of it. It wasn’t a rupture from the old economic system, and it continued to enrich the same socioeconomic classes and the same vested interests to this day. It was always extractive, always serving the elite, always serving the interest of the former colonial interests. The question today is, you look at the accumulation of trade deficits and external debt because we were told, “well, you know, your economy is mostly extraction of resources and agriculture. You should diversify and you should invest in manufacturing and industrialization.” You try to industrialize and there’s a huge technological gap. So, what do you do? You go through an early phase of sort of import substitution industrialization in the 1950s and 60s. Basically, most developing countries did that under protectionism, which is protection from foreign competition.

But then, ten years later, you’re told “That’s it. Your infant industry is not infant anymore. So now you should move into export led growth. Good luck exporting.” When you move into export-led growth in the 1970s, one of the first things you notice with every single country that went through this phase is that the trade deficit explodes. You would think, if we were going into an export oriented mode, we should be thriving through exports. It turns out you end up importing even more, because your economy is not highly industrialized, you end up importing all the intermediate goods and all the technology and all the input that goes into your assembly line’s basic manufacturing system.

So you’re importing high value added content and you’re exporting low value added content. You’re just adding the kind of very basic assembly line skills to export a finished product. If you’re importing more than what you’re exporting, your trade deficit is exploding, how do you finance this trade deficit now that it’s putting pressure on your exchange rate and it’s going to turn into food riots and fuel riots and all kinds of instability? You borrow.

That’s where the external debt comes in. You borrow based on the idea that when you grow even faster in the next decades, you’ll be able to pay it off. It just never happens because you’re never industrialized enough to compete internationally. This whole era of opening up to free trade and globalization has been a massive trap for developing countries that actually led to even more loss of financial sovereignty over time, directly after independence. The way to undo this or to regain or reclaim monetary sovereignty is to look at the specific cases. There’s no cookie cutter approach to this. Every country has its own institutional specificities and needs. So you look at what is causing the external debt, what is really driving it?

Is it food imports? Is it energy imports? Typically, it’s both for most countries, with the exception of oil exporting countries. The third category is typically what I described as low value added content of exports relative to the high value added content of your imports. So, if you’re going to reclaim your food sovereignty so you don’t have to borrow as much to buy food from abroad, then the only way out is investment and sustainable domestic agricultural policy.

This is something that the West recognized from the beginning. This is not something that I discovered or people discovered in the last few years. If you go back to the free trade negotiations, the GATT (General Agreement on Tariffs and Trade) and other trade negotiations in the 50s and 60s and 70s, and to this day, the West will always negotiate free trade in everything but arms and farms.

No weapons and no food, because that’s national security for the West. It’s not just national security, because you need food during wartime. It’s because you lose your sovereignty. You lose part of your sovereignty if you’re dependent on other countries for your national security, for your food security. I’ve known this for a long time, but MMT really put a new light on this particular issue.

You find the European Union and the United States putting really impossible conditions in these trade negotiations, making it impossible for developing countries to export food.In the case of Europe, a lot of the former colonizers were dependent on food imports from North Africa and other parts of the world. That wasn’t going to be fun, economically speaking, after independence, because now you depend on these newly independent nations for your food supply. CAP, which is the Common Agricultural Policy that the EU put in place, was virtually a ban on food imports and also a massive subsidy for European farmers to build up capacity and depend less and less on imported food.

That ends up killing agriculture in a lot of developing countries. When you kill agriculture in developing countries, you’re forcing people to move out of rural areas into urban areas, which was pretty convenient because the cheap labor from manufacturing assembly line jobs was waiting for them, because that was the era of export-led growth. Developing countries become the tail end of the supply chain in the global supply chain system, because they’re just the assembly line for all the high value added content that’s been produced through the rest of the supply chain. It happens to be convenient because it creates a little bit of jobs in developing countries, but never enough to truly industrialize those countries or truly develop those countries or bring prosperity. I hope this clarifies the links between Europe and former colonies in Africa.

Scott Ferguson

It does. Can you talk about some of the dangers of potential inflationary pressures? I know in your own work you stress a strong political movement, but also, sometimes a very careful and strategic economic development approach.

Fadhel Kaboub

Yeah. The strategic economic development approach to reclaim monetary sovereignty is renewable energy production, because that’s another major component of the external debt, sustainable food policy, because that’s the food imports problem that many developing countries have. Then the third one, which is a more difficult strategy and takes a long time, is investment in education and vocational training and technical skills, because if you want to industrialize and move up the ladder over time, so to speak, in value added content, the only way you’re going to attract manufacturing that produces higher value added content is if you have the infrastructure, in terms of electricity and telecommunication and transportation, but also the highly qualified labor that’s required to be plugged into the production of high value added content. That takes time. It takes a couple of generations to move up the ladder. Those are the three strategies that I always emphasize.

The question is, “well, can we make the transition overnight or in a decade?” To me, the answer is not that it’s not going to happen overnight or in a couple of years, but at least you have to start thinking about that direction, planning for that direction, and then shifting resources away from your old strategy into your new strategy. The current strategy, for example, is to subsidize food and food imports and to subsidize energy imports because you’re importing fossil fuels at globally determined prices, which can be inflated for your local consumers. If you don’t subsidize them, you’re going to have fuel riots. If you don’t subsidize imported food, you’re going to have food riots. So, governments typically subsidize and offer food and fuel and transportation at affordable prices locally.

The idea here is to shift some of the subsidies away from subsidizing fossil fuel and imported food into building more productive capacity of renewable energy production and sustainable food production and, over time, accelerate that shift and accelerate the development of those resources, because that’s the ultimate way of reclaiming energy sovereignty, food sovereignty and, as a result, monetary sovereignty.

Scott Ferguson

And as a result, political sovereignty.

Fadhel Kaboub

Absolutely, because you become less dependent, financially, on the outside world. As a result, you are more politically independent and, to be honest, that’s been recognized from the beginning by former colonizers as a threat. It was clear that having this neocolonial way of controlling former colonies through the financial aspect is way more effective than having troops on the ground, controlling the economy and policing the population, because it gives you the illusion of political independence. You have your flag and you have your football team and you have your territory, your military, and will even give you aid to help you reinforce your territorial sovereignty and police your population and everything. It feels like, “yeah, we have independence.” When it comes to economic reality, you’re not independent.

As a result, politically, you’re constantly under manipulation by the lenders and, typically, countries who are the former colonizers. That’s really the part that the average person doesn’t necessarily realize, but political elites know this and they know that they can use it to their advantage. They’re not really, in most cases, willing to take on the challenge of challenging the external forces, especially when it’s not a democratic system. They’re actually kept in power with the help of external forces. This was definitely the case with the Ben Ali regime. It wasn’t a secret or anything. If anything, during the days of the uprisings in 2010, 2011, the French Minister of the Interior was vacationing in Tunisia with the president’s family and called France to approve more shipments of tear gas for the police to handle the protesters.

The only reason why the tear gas didn’t make it to Tunisia, because workers at the airport were on strike in France. It had nothing to do with the political agreement between Tunisia and France. It was just a coincidence that the workers were on strike. When you travel through Paris and workers are on strike, you don’t get your luggage. So, the tear gas never made it.

Maxximilian Seijo

Something that’s been in the news that is really evocative of what you’re describing is the question of currency unions and the way they determine political and economic relations. However, a lot of attention has been paid to the eurozone crisis in Greece and Italy and Spain and the political unrest that is resulting from that.

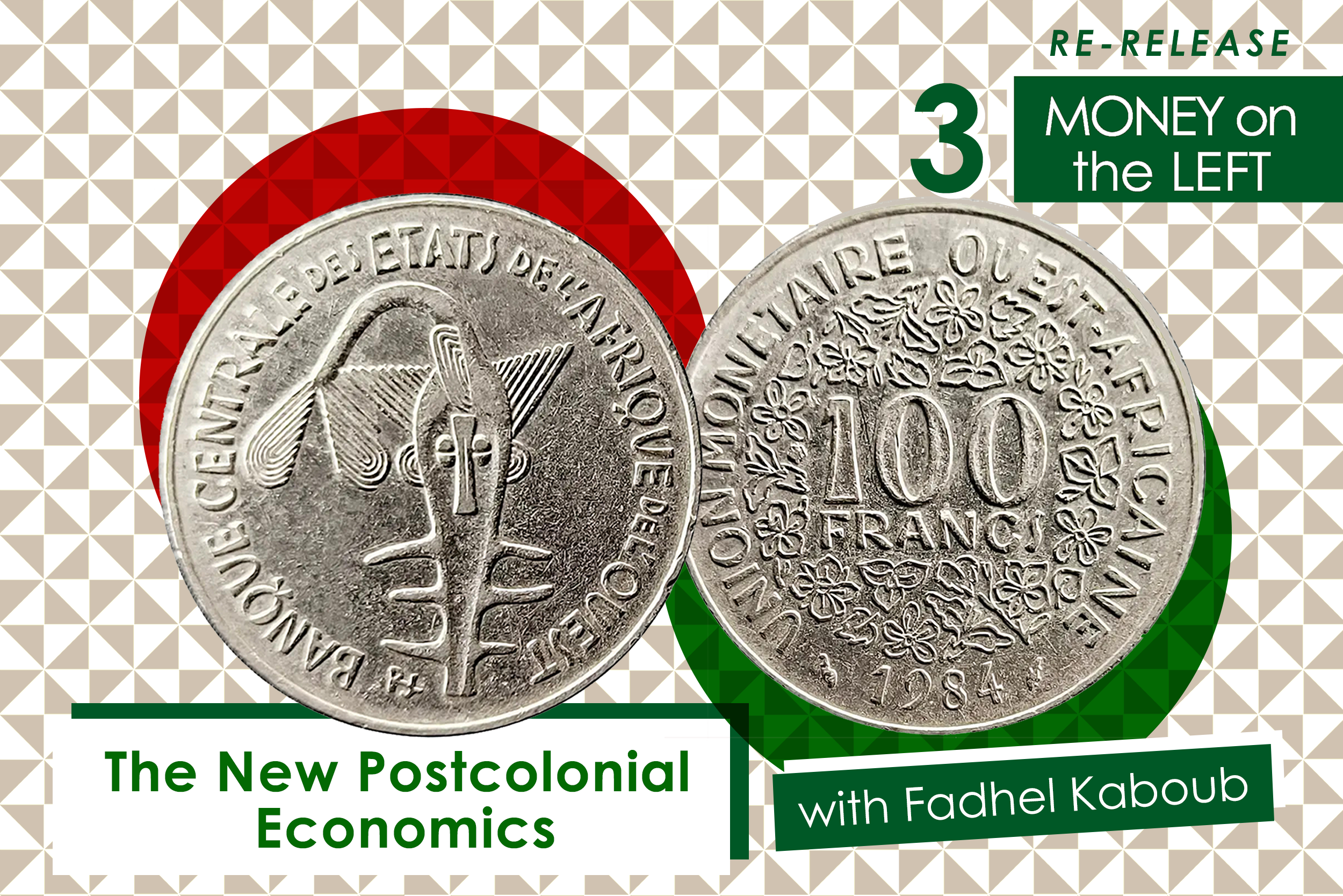

I was wondering, though, if we could talk about a currency union — if you want to call it that — that gets a lot less attention, the CFA franc (Communauté Financière Africaine, or “African Financial Community”). If you could tell us about the history of it and the structure of the CFA franc today.

Fadhel Kaboub

The CFA franc is a currency used in Africa. Today, it is used by 14 countries, mostly former colonies of France. The name of the currency union changed over time. Mostly to make the name more politically correct, I guess. CFA used to stand for — trying to remember the French name — Colony Francis d’Afrique, which means the African Colonies of France. That’s what CFA used to stand for. It was clearly stating that these are the colonies, and they use the French franc, but this is the African version of the French franc. It’s controlled by the French government and by the French authorities. After independence, you can’t call these colonies anymore. At some point, it changed its name from Colony France’s d’Afrique to Communauté France’s d’Afrique, which was a little bit more politically correct. Today, it’s called Communauté Financière Africaine, which is the African financial community or union. It doesn’t carry the colonial name anymore, but it still operates under the exact same institutional setting, which is a currency union for 14 countries today.

It was created in 1945, right when a lot of the former French colonies were gaining independence, but they were not transitioning to a national currency. Most colonies during a few years after independence continued to use the same colonial currency. But in the case of the West African and Central African countries, the 14 countries that remain in that union today, they transitioned into the CFA franc. When you think of monetary policy and fiscal policy and exchange rate policy, it’s all determined by the French government, essentially. I mean, there is a committee and there’s a board and there’s some sort of bureaucratic structure to it that’s staffed by representatives from the African nations. Presumably, they get to make their own decisions and vote, but we all know that it’s nonsense, that it’s set up by the French government.

I mean, Macron has been under fire in the last couple of years, especially during his visits to Africa, because there’s lots of protests against it. Students brought it up during the open Q&A session and he keeps brushing it off and saying, “well, no, but I’m not standing in the way of any country to leave the CFA if they want it,” or “we don’t control it.” If anything, he sees it as a way of cooperation and assistance to help stabilize the monetary system of the 14 countries in the union. In terms of our experience, knowing what monetary sovereignty means from an MMT perspective, you clearly understand that a group of countries that use a single currency that follows a particular set of monetary policy rules has a very limited fiscal space to engage in strategic economic development internally. Everybody’s familiar with the situation in Greece and Italy and Spain after the euro crisis, when you have a central bank like the ECB (European Central Bank) that refuses to allow any of their member countries to deal with the economic crisis and imposes austerity on those countries. You can think of the CFA franc system in exactly the same setting. 14 countries joined in a monetary union that have no way of issuing their own currency, and they peg their currency to the euro today. It used to be the French franc, which was pegged to the dollar indirectly, via the gold standard at the time.

You can understand how much economic development has been withheld and how much economic sovereignty has been withheld from these countries. Unfortunately, it took decades for this beginning of a movement to start building in the last few years. I think MMT has a lot to contribute in this regard. I’m looking forward to working with some of our new MMT-ish friends in this movement to build a coherent narrative or coherent counter argument to the CFA and to and to bring about an alternative.

I don’t think this is going to be done through the political elites. I think it has to be done through a social movement. I don’t really believe in political leaders, quote unquote. The political leaders are not leaders, they’re really followers when it comes to these things. It has to be a social movement that builds a coherent narrative, a coherent critique, and a coherent alternative. When you get to a critical mass of people, of the media, of academics who engage in a coherent way, that’s when political leaders really take action and become followers when it comes to this.

Scott Ferguson

Do you have a sense of the way that the eurozone currency project compounds the problems of the CFA franc?

Fadhel Kaboub

If you’re economically dependent on France and the eurozone for your economic well-being and the main unit — the eurozone — is going through a crisis, you suffer the consequences. There’s a direct link to this, and ironically, this is really what woke up a lot of people to the reality of the connection between CFA and Europe. It was ironic because it wasn’t really in the MMT way. A lot of people were saying, “well, the gold reserves of the CFA countries are in France, and the French are probably using that to deal with their economic crisis,” but it did raise awareness about the issue. Obviously, to you and me understanding MMT, it’s really not about the gold. For a lot of people in these countries, they say, “well, we’re the largest producers of gold in the world. Where is our gold? It’s held in France. And why is our economy not doing so well?” But, it’s not because the gold is in France. It’s because the economy is producing raw materials and raw materials are very low value added content.

You don’t get to control the price of those raw materials in the global system. So, no matter how much you produce of your raw materials, even if you are the number one exporter of this particular commodity, you’re still not going to be reaping the benefits of it. You can think of this in terms of African countries or North African countries. I know this specifically for Tunisia, because Tunisia is one of the largest producers of olives in the world. Depending on the season, it’s number three, number four, or sometimes number two, but it doesn’t get any of the publicity of being an olive oil country. When you think of olive oil, it’s Italy, it’s Spain, or Greece, maybe Turkey, because these are the distributed brands that you pick up in the supermarket.

They’ve done a better job at controlling the global supply chains and branding their product. Most of the price that you pay is for the bottle, it is not for the olive oil, it’s for the PR that goes with it, the advertising that goes with it. It turns out that, for the average Tunisian farmer that’s producing the olives, they end up selling their entire year’s worth of olives a year in advance at a set price determined by an Italian company or a Spanish company. When you look at how much of the market, Spain and Italy, collectively control, they essentially have, last time I checked, 4 or 5 years worth of the global supply of olive oil in reserve. If you’re a small farmer and you don’t want to sell at a set price, they say “Keep it. Good luck. Good luck selling it because we have enough to supply the entire world for the next five years.” As a farmer, no matter how big you are, you can’t afford to negotiate. This is true for all kinds of farmers in Africa.

When you think of chocolates, what’s the main input? Where does it come from? It doesn’t come from Switzerland. It comes from African farmers who don’t get to control the supply chain. They don’t get to control the price. They’re at the lowest end of the supply chain in terms of value added content. Who gets most of the benefits? It’s the companies that add that value added content, which is the pretty bottle, or the fancy designs, or the nice chocolate boxes that most customers in the West pay most of the price for, not for the actual raw material.

There’s a structural economic development problem in the CFA region in particular and yet the recognition of the economic problem came through the crisis in Europe and the thought that the gold was in France and that’s why things are messed up. It’s about beginning a conversation with colleagues and activists and journalists about what MMT has to offer about this. We’re shifting the narrative to the real structural problems, not just the fact that gold is stored in France.

Maxximilian Seijo

You know, talking about these global issues and the story you just described about the olive oil, it makes me wonder, if we’re going to reimagine what development looks like in a global economy, is there any role for an intergovernmental authority like the United Nations to play in the process of further decolonization?

Fadhel Kaboub

Yeah. There were several attempts to do this over the years. You can guess, it’s not the IMF (International Monetary Fund) and it’s not the World Bank. Good guess. These are technically agencies of the UN, it just happened to be the more politically and financially powerful organization of the UN. Within the UN, the organization that has done the most in this regard is UNCTAD, which is the UN Conference on Trade and Development. I’m probably biased here a little bit, but especially when Jan Kregel was in charge of writing the UNCTAD annual reports and organizing the UNCTAD conferences.

Kregel is one of the leading post Keynesian economists, and one of the most brilliant economists, period. Also, his work with the UN and his understanding of Keynes and MMT in the global financial system led him into what I described. A lot of the things that I’ve learned about economics and MMT, I’ve learned from Jan Kregel, obviously. You hear a lot of his thoughts from me. In anything that’s a bunch of nonsense, it’s probably my thinking, not his thinking. He and other economists at UNCTAD have probably done the most to rally developing countries to think differently and to act differently.

But, if you ask Kregel, and I’m not going to speak for him here or put words in his mouth, you’ll hear a lot of stories about how much pressure UNCTAD as an organization gets from the West, from the US in particular or how much pressure representatives of developing countries who really begin to learn from the UNCTAD approach and attempt to act accordingly come under. You have to realize that the process of international development is not done in isolation from geopolitics. You’re at the UN and you’re negotiating economic development issues with other governments who also happen to be negotiating all kinds of other things with you and all kinds of other things with other allies that have nothing to do with you.

Somehow your vote in the Security Council matters on a particular issue. So, you get a lot of pressure if you attempt to align yourself with the other developing countries who happen to align themselves with Cuba, for example, then you’re with them, not with us, and you’ll suffer the consequences. You have to remember that you’re doing this in the context of massive external debt. You’re dealing with all kinds of problems, including maybe a potential civil war, including potential rebels, including potential unrest because of food prices going up. You’re extremely vulnerable to pressures from the West. If you attempt to gradually pull yourself out of the dominant structure that you’re suffering from, it takes time to build an economic development strategy and put it in place and during that time you need some sort of immunity from all kinds of other threats and interferences and pressures. That’s the reality of it. There is no such thing. That’s why a lot of economists and people who are thinking about the geopolitics of this say when when the Cold War ended it made this even more difficult, because for developing countries at the time, they could sort of fall in between the East and West and kind of leverage and play a little bit of the geopolitics between the Soviets in the Americans to get a little bit from both. But now that we live in a world that’s exclusively dominated by US interests and in US power, geopolitically, there is no negotiation. There is no running away from that kind of influence. The only way out of this is to start building South-South regional cooperation, economic development units and it’s very difficult politically and economically because you have to agree on a joint strategy. To get a number of countries to agree on a particular strategy is very difficult.

To then also get a group of countries that have complementary assets and resources to coordinate is difficult. At some point there was a little bit of hope that BRICS will emerge as that geopolitical alternative. BRICS, as in Brazil, Russia, India, China and South Africa — the “S” was added eventually as South Africa — as an alternative to the US geopolitical dominance. I don’t know how likely that is going to actually emerge because the BRICS itself as an organization has been divided over the last few years. In the absence of a block of countries that have geopolitical influence that can offer an economic alternative, it’s very hard for developing countries to shift strategy. There is the possibility that the Chinese model of economic development and China’s interest in the rest of the world, economically speaking at least now, may offer a little bit of relief.

But, you also have to take that with a grain of salt, because China also has its own economic and geopolitical interests that it’s trying to build up to being a superpower — a true superpower. You have to take anything that comes from the Chinese government also with a grain of salt. A fistful of salt, I should say.

Scott Ferguson

So you’ve done some consulting work with various governments and groups in, what we call, the Global South. Can you talk a little bit about those experiences, what you’ve learned and general lessons from that work?

Fadhel Kaboub

Yeah. So, just to clarify, when you say consulting, I don’t have any official affiliation or paid positions with any government in the Global South. By consulting, I mean people reach out and want to ask questions and have long conversations or presentations. So, yes, I’ve done that, but not as a paid consultant for any government.

Scott Ferguson

Understood.

Fadhel Kaboub

Most of the interest is what we described today in this podcast, which is, we recognize that everything we’ve tried has failed. All of the stages of economic development that every textbook follows, including the most recent waves of privatizing state owned enterprises, leaning heavily on tourism, foreign direct investment, and export led growth.

The MMT lens and the sort of UNCTAD economic development analytical lens allows us to recognize that those are traps, because the more you accelerate your exports, the more you end up with imports of intermediate goods. You’re never going to catch up. The more you privatize state owned companies to generate dollars to pay some of your external debt, once you privatize the water company, you can’t reprivatize it the next year.

It’s just a one off, and then you lose that asset, and then you run out of assets to privatize. Of course, you also lose control over strategic resources in your own country. The idea of foreign direct investment is also a trap for most countries because you realize most foreign direct investment actually goes to rich countries, not to poor countries, because it’s looking for strong infrastructure, water, electricity, transportation, telecommunication.

Most developing countries don’t have that. Also, foreign direct investment is looking for skilled workers and highly qualified workers. Most of those happen to be in Canada and the Netherlands and other places, not in the poorest countries. This idea that foreign direct investment is going to solve all the development and poverty problems is a myth because we use China and India as examples of great places that attract foreign direct investment. But those are not your usual developing countries because they have massive infrastructure of telecommunication, transportation, everything else and they haven’t invested massively in producing the labor force that FDI is looking for. You look at most of the developing countries, it’s really assembly line jobs, the tail end of the supply chain at the lowest skill levels, the lowest value added levels. That’s not going to work.

That’s the context within which a lot of progressive voices within those governments — or not necessarily progressive, just eclectic and pragmatic individuals — try to reach out for alternative ideas. We then start having conversations like the one I just had with you, and then we get into the geopolitical stuff. That’s when they realized this is going to be a problem because this is not just a technical solution. This is a political economy framework that has to be undone. It starts with a lot of education leading into a social movement and this is really where having these conversations with colleagues in Mexico and in Colombia, in other places comes in.

They say, “we don’t really have what you guys have,” for example, in the US, which is kind of the beginning of a movement. The groups like real progressives and all kinds of people in all kinds of walks of life. Not academics, not professors, people who are working 9 to 5 jobs but who are very passionate about public policy, who now understand the issue and can argue and offer a counter narrative and can stand in front of a senator or representative and say, “you can’t trick me into this because I know better, and I can argue back and I can even educate you on what the solutions might be.” So we’re at the beginning phase of building a popular movement of people who can actually argue back against the senator or representative. And they say, “we don’t really have that yet, and we don’t have that kind of social movement. We have a few academics and a few activists, but it’s not a movement yet.”

A lot of the conversation eventually shifts into working on multiple fronts. Beginning a conversation with academics, which is the most difficult one, to get academic economists to think differently. Then you start working with progressive policymakers who are not necessarily dogmatically wedded to neoliberal ideas or neoclassical ideas to start to show the potential of these ideas, and working on social media and working with popular media to popularize the ideas in the public domain and engage with the usual suspects; with labor unions, with activists, with climate justice activists and social justice activists to say, “look, we’re allies on this thing. We have a solution. This is a solution that empowers your organization and your message to build a united front against neoliberalism.” This is how you build a movement. As I said earlier, politicians are the last people to follow because you talk to them behind closed doors and they understand. They say, “Well, that makes sense, but I can’t say this publicly because I get attacked by all kinds of media and other political parties say, ‘you don’t know anything about inflation, you want to turn this into Zimbabwe,’” or whatever. If you’re the only one trying to counter that, it’s difficult. So they say, “get me a critical mass of people who endorse this.” In other words, “get me a social movement and I’ll come out and embrace it.” I always joke, I say, “Well, you know, if I have a social movement, we’ll vote you out of office. We don’t need you.” That’s the reality, but we can’t give up.

As I said, you have to work on multiple fronts. We’re not saying that everybody has to come out and say, “I’m an MMT candidate, and I endorse this and that and the other.” Just start shifting the narrative and make common sense decisions and parliaments. When you’re being asked to look at foreign direct investment options, just be more selective. Go for the higher value added content. Try to negotiate a little bit better, when it comes to dedicating resources to subsidizing fossil fuels versus domestic renewable energy infrastructure, make the right decision, move away from fossil fuels no matter what the pressures are and think of strategies of building energy sovereignty and food sovereignty.

You don’t have to say this is MMT. You don’t have to say this is inspired by UNCTAD or anybody. This is just common sense. So, that’s where policymakers can be more effective just by making commonsense decisions that fit into the broader strategy that I described. But again, we have to work on multiple fronts. That’s why we were really fortunate to have the opportunity to create the Binzagr Institute, because we didn’t want this to be stuck in academic circles, because we’ve done that for a long time. As I said, we don’t think that’s how the world is going to change. It’s not going to change in academic journals that publish rejoinders. I like rejoinders, but they’re not going to change the world.

Scott Ferguson

Indeed. Well, this has been incredibly informative and engaging, Fadhel. Thank you so much for joining us on Money on the Left.

Fadhel Kaboub

It’s a pleasure. Thank you.

* Thank you to Robert Rusch for the episode graphic, Nahneen Kula for the theme tune, and Thomas Chaplin for the transcript.